The definitive guide to SEPA bank transfers for businesses

2026-02-04

If you have ever had to pay an invoice to a supplier in another European country, you will know that it used to be a real headache. High fees, uncertain timelines, bureaucracy… It was a full-blown international operation. Fortunately, all that changed with the arrival of SEPA bank transfers.

What SEPA transfers are and how they make your life easier

In short, a SEPA transfer is a payment in euros that moves through the Single Euro Payments Area (SEPA) as if it were a domestic operation. It makes no difference whether you send money to a supplier in Germany or a client in Portugal: the process is exactly the same as if you were sending it to an account in your own city.

Think of SEPA as a common “language” that all banks in the area have agreed to speak. This system unifies the rules of the game, technical formats and costs, removing the old barriers that complicated cross-border payments.

The real impact of SEPA on your day-to-day business

This standardisation has been a game-changer for the financial management of thousands of businesses. Now, paying an invoice to a supplier in Paris, Rome or Lisbon is as simple and cheap as paying the one next door.

The benefits are direct and noticeable from day one, especially for SMEs:

- Cost savings: The regulations are clear: a SEPA transfer cannot cost more than a domestic one. No more abusive fees for international payments within the zone.

- Predictable cash flow: Timelines are guaranteed. A standard transfer arrives, at most, by the next business day. This gives you total control over your cash flow.

- Simplified management: You can centralise all your euro payments and collections from a single bank account, regardless of which country your clients or suppliers are in.

SEPA is not just a set of technical rules. It is a tool that breaks down financial borders and turns Europe into your local market.

In practice, this system transforms a market of 36 countries into a domestic space for your finances. This opens up a world of possibilities: hiring talent abroad, collaborating with suppliers across Europe or selling to clients in any country in the zone without payment friction. Complexity disappears and only efficiency remains.

For a clearer picture, here is a summary of the key concepts.

The SEPA system at a glance

This table summarises the fundamental elements of the SEPA system so you can quickly and clearly understand its impact and how it works.

| Concept | Description |

|---|---|

| Definition | Single Euro Payments Area. A space where citizens and businesses can make and receive euro payments under the same conditions, rights and obligations, regardless of country. |

| Geographic scope | Includes the 27 EU countries, plus Iceland, Liechtenstein, Norway, Switzerland, Monaco, San Marino, Andorra, Vatican City and the United Kingdom. |

| Main objective | To eliminate differences between domestic and cross-border euro payments, creating a single, efficient market. |

| Key instruments | Transfers (SCT) and Direct debits or standing orders (SDD), both standardised under the same technical format. |

As you can see, SEPA is much more than an acronym; it is the engine driving a truly integrated European market.

SEPA transfers vs. direct debits: which do you need?

When we talk about SEPA payments, we are actually referring to two main tools that, although they may seem like cousins at first glance, perform completely opposite functions: transfers and direct debits. Understanding what each one is and what it is for is key to avoiding confusion and managing your business cash flow like a pro.

The fundamental difference boils down to one simple question: who initiates the movement of money?

Think of a SEPA transfer (technically known as SEPA Credit Transfer or SCT) as a “push” payment. That is, you are the one who takes the initiative and “pushes” the money from your account to someone else’s or a company’s. You give the order to send.

Conversely, a SEPA direct debit (SEPA Direct Debit or SDD) works like a “pull” collection. In this scenario, it is the company that will collect that “pulls” the money from the client’s account to its own, always with prior permission.

SEPA transfers: total control to pay

Transfers are your day-to-day tool for making payments, whether a single one or an entire batch. They are the digital version of handing over cash. You decide when, how much and who to pay.

They are the perfect tool for: * Paying salaries: At the end of each month, you send the salary to your employees’ accounts in bulk. * Settling supplier invoices: An invoice arrives for a service you have received and you pay it. * Making one-off payments: Buying new office supplies or paying an extraordinary tax.

In all these cases, the action starts with you. You have absolute control over when the money leaves your coffers, giving you very precise visibility and control of your cash flow. SEPA bank transfers are, in short, the standard instrument for meeting your payment obligations.

SEPA direct debits: automation for collecting

With direct debits, the picture changes completely. They are the ideal solution for automating recurring collections and giving your business a predictability of income that would otherwise be impossible. But beware: to do so you need a signed authorisation from your client. This document is the famous SEPA mandate.

What is a SEPA mandate? It is the contract that gives your company legal permission to initiate collections from a client’s bank account. Without a valid, signed mandate, you cannot issue a single direct-debit collection.

This model is a lifeline for businesses with predictable income: * Subscription fees: You collect the monthly fee from users of your software, platform or service. * Periodic collections: You manage the collection of gym fees, community fees or accounting firm fees. * Instalment payments: You automate the collection of the different instalments of a financed product you have sold.

Direct debits put you in the driver’s seat of your collections, drastically reduce late payments and save you the hassle of chasing clients to pay. And for the client, it is pure convenience: they forget about having to make a manual payment every month.

Understanding the technology that makes SEPA payments work

For a SEPA transfer to work with Swiss-clock precision, there needs to be a common language that all European banks understand. Although it may sound complex, it is actually based on a couple of key identifiers and a standard file format. Think of it as the GPS coordinate system for European payments: it ensures that money always reaches its destination without going astray.

IBAN and BIC: the coordinates of your money

The first pillar of this system is the IBAN (International Bank Account Number). It is not just a longer account number, but an intelligent code designed to prevent errors. Its structure, which always starts with the two letters of the country (ES for Spain, DE for Germany, etc.), followed by two check digits, allows instant automatic validation. This small detail drastically reduces typing errors, ensuring that funds go to the correct account from the start.

Alongside the IBAN, the BIC (Bank Identifier Code) or SWIFT was always used. This code is like the “postal address” of the receiving bank. However, one of the great advantages of SEPA standardisation is that for most operations within the zone, the system already knows which bank an IBAN belongs to without needing more data. That is why for SEPA bank transfers between member countries, the BIC is usually no longer mandatory, which simplifies things a little more.

The XML format: the universal language of banks

When a company needs to pay salaries or suppliers, it does not make hundreds of transfers one by one. The norm is to prepare a single file with all payment orders and send it to the bank. This is where the ISO 20022 standard comes in, an XML-based file format that has become the mandatory norm for all banking communications in the SEPA zone.

Forget about spreadsheets or plain text files that each bank interpreted in its own way. XML organises information with clear tags, so that banks’ computer systems read and interpret it without any ambiguity. For transfers, the most common file type is called pain.001.001.03.

Think of the XML file as a universal digital form. It contains all the data organised in labelled boxes that your bank can process completely automatically, eliminating manual intervention and the errors it entails.

Understanding what information this “form” contains is key if you want to automate your payments. Inside the file, each individual transfer must include essential fields for the bank to accept it. Let us see which are the most important.

Essential fields in a SEPA XML transfer file

Below we break down the essential data that a pain.001 file must contain for your bank to process it without problems. If your management system (ERP or CRM) generates these files, make sure it includes this information.

| XML field | Data description | Practical example |

|---|---|---|

DbtrAcct/Id/IBAN |

The IBAN of your bank account, the one that orders the payment. | ES9121000418450200051332 |

Cdtr/Nm |

The full name of the beneficiary or the company name of the company receiving the money. | ACME Ltd. |

CdtrAcct/Id/IBAN |

The IBAN of the recipient’s bank account. This is the most critical data. | FR7630006000011234567890189 |

InstdAmt |

The exact amount of the transfer, indicating the currency (always EUR for SEPA). | 1250.75 |

RmtInf/Ustrd |

The payment reference. The text that the recipient will see on their bank statement. | Invoice payment F-2024-0089 |

As you can see, the structure is quite logical. Making sure these fields are properly completed is 90% of the work to get your transfer batches processed without incident.

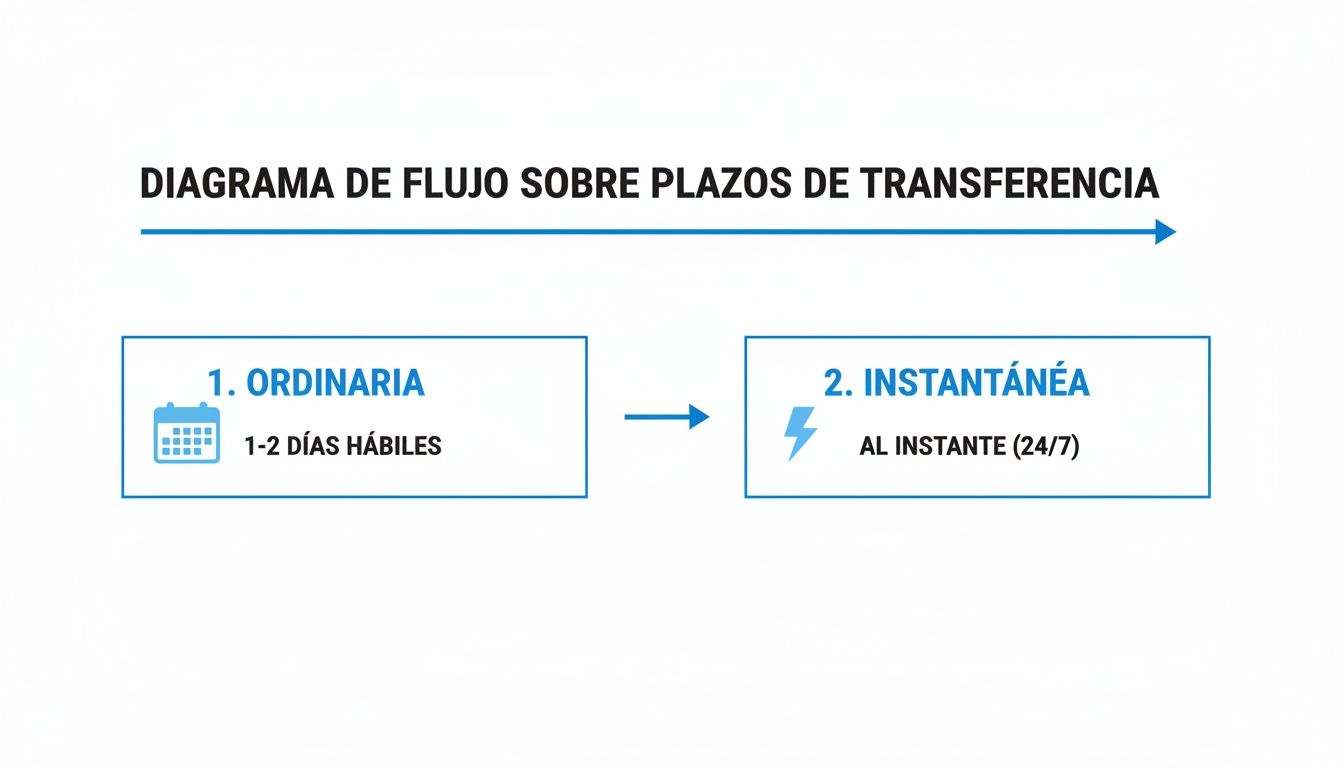

Timelines and costs: ordinary vs. instant SEPA transfers

When we manage payments, two questions always run through our heads: how long will it take to arrive? and how much will it cost me? In the world of SEPA bank transfers, the answers are fairly clear and, fortunately, usually work in favour of your business agility.

The key is knowing how to choose between the ordinary and the instant transfer. Each has its moment and its reason for being, and understanding them well will help you make better decisions for your cash flow.

Ordinary SEPA transfers: the trusted standard

Think of the ordinary SEPA transfer (SCT) as the reliable payment method of a lifetime. It is the workhorse for most operations in Europe. Its great strength is predictability: by regulation, the money must be in the destination account, at the latest, by the end of the next business day after issue.

But beware, there is an important detail you should know: your bank’s “cut-off time”. Each institution sets an afternoon deadline. If you launch the transfer before that time, it counts as done that same day. If you miss it, for all practical purposes it is as if you had done it the next day, which delays the arrival of funds by a full day. You can learn more about how timelines and cut-off times work in our detailed guide.

As for cost, SEPA regulation is very clear: a euro transfer to another country in the zone cannot be more expensive than a domestic one. For most businesses and self-employed, this means that fees are very low or, directly, zero.

Instant SEPA transfers: speed comes first

What happens when waiting a day is not an option? This is where instant SEPA transfers (SCT Inst) come onto the scene and change everything. The money arrives in less than 10 seconds. And the best part: it does not matter if it is at night, weekend or bank holiday. They work 24 hours a day, 7 days a week.

This immediacy is an incredibly useful tool for cash management. It allows you, for example, to pay a supplier on the spot so they release goods or to solve an unexpected payment without the typical bank wait.

The new European regulation is giving a definitive push to instant transfers. Soon, banks will be obliged to offer them at the same price as ordinary ones, removing the cost barrier. This will undoubtedly make them the new standard for many day-to-day payments.

The rise of this type of payment is unstoppable. In Spain alone, 1.556.3 million instant operations have already been exceeded in one year, representing growth of 31.1%. This figure puts us as leaders in Europe and shows that immediacy is no longer an extra, but something we all expect in our finances.

How to automate your bulk payments and generate SEPA files

If you have ever had to manage salary payments or settle invoices to a host of suppliers, you know perfectly well that it can become a real administrative bottleneck. The real challenge is not having the list of payments, which is usually already in an Excel or CSV, but converting that list into a SEPA XML file that your bank will accept without question.

Trying to create these XML files by hand is, to be honest, a rather tedious and error-prone task. It requires knowing the ISO 20022 regulations inside out. A small mistake, such as a tag that is not closed properly or data in the wrong place, and the bank will reject the entire batch. The result: delayed payments, possible rejection fees and a good dose of frustration.

The solution: specialised conversion tools

Fortunately, you do not have to fight with XML code. There are tools designed just for this, which act as an expert translator between your spreadsheet and the technical language your bank understands.

The process could not be more straightforward and efficient: 1. Upload your file: Simply export the payment data (IBAN, name, amount, reference) from your management programme or organise it in a simple CSV or Excel file. 2. Map the columns: You tell the tool which column in your file corresponds to each SEPA field. It is as easy as saying “column A is the IBAN” and “column C is the amount”. 3. Download the XML: Instantly, the platform delivers a perfectly assembled and validated SEPA XML file, ready to upload to your online banking. For an extra safety net you can also run the file through our SEPA direct debit XML validator before submission.

The good thing about these tools is that they completely eliminate the risk of format errors. They take care of all the technical complexity, allowing you to have a SEPA bank transfer file ready in minutes instead of hours, with the peace of mind that the bank will accept it first time.

Full integration via API for developers

For companies that want to go one step further in efficiency, automation can be total. Development teams can integrate this functionality directly into their own systems (ERP, CRM or any custom software) using an API.

This means that SEPA XML file generation becomes a process that runs on its own. Imagine that when you close the month’s billing, the system automatically creates and sends the supplier payment batch without anyone having to intervene. If you are interested in this approach, you can check what data your transfer CSV file must contain to make integration a success.

Automation not only frees up valuable time, but also minimises the risk of human error. In the end, it is about ensuring that your business payment cycle is as agile and reliable as possible.

How SEPA automation is applied in your company’s day-to-day

Now that we have seen the technical side, let us get to the interesting part: how can SEPA bank transfer automation really change the operations of different businesses? Because beyond the theory, the real value is in seeing how it solves real problems and gives us back time for what really matters.

Putting yourself in the shoes of these examples will help you see how you could apply these solutions to be more efficient and, in passing, avoid more than one headache.

A breath of fresh air for SME operations

Any small or medium-sized company knows how many payments it manages every month. Imagine if the administration team could automate the payment of all salaries. Instead of making each transfer one by one, they simply generate a single batch file and that is it.

The same goes for suppliers. Just export a list of pending invoices, create the XML file and settle payments to dozens of them in one go. This small change frees up a huge amount of hours that were previously spent on manual, repetitive tasks, minimising the risk of silly typing errors that can delay payments and damage the relationship with a good supplier. If you want to start with the basics, it is useful to know how to convert transfers from CSV to a SEPA XML file, as this is usually the most common starting point.

Everything centralised for accounting and advisory firms

Accounting and advisory firms are the nerve centre of accounting and payments for many clients. SEPA automation is a powerful tool for them, as it allows them to centralise the management of direct debit and transfer batches in a much more agile way.

An advisory firm can prepare from a single platform the files to collect payments for all its clients, validating the data and ensuring that everything complies with regulations. This not only saves them time, but also allows them to provide a more reliable and higher quality service, reinforcing their role as a trusted partner for their clients.

Full integration for developers and SaaS

For a developer or software company (SaaS), the magic word is API. By connecting their system to an API, they can generate SEPA files in a fully programmatic way, without anyone having to intervene.

A good example is a SaaS that works by subscription. It could automatically create each month the direct debit files to collect from all its users. This completely eliminates the manual work of the collection cycle, guarantees a predictable income flow and allows the system to grow without problems, whether they have a hundred clients or a hundred thousand.

We answer your questions about SEPA transfers

No matter how standardised the system is, the same questions always arise in day-to-day operations. Let us clear up the most common doubts about SEPA bank transfers so you can operate with complete peace of mind.

Here you will find direct answers, the kind that get straight to the point, on topics ranging from the geography of payments to what to do when things do not go as expected.

Which countries are part of the SEPA zone?

Many people are surprised to discover that the SEPA zone goes far beyond the European Union. Of course, it includes the 27 countries of the EU, but the list goes on. Iceland, Liechtenstein, Norway, Switzerland, Monaco, San Marino, Andorra and Vatican City are also included.

A key fact, especially after Brexit, is that the United Kingdom remains part of the SEPA scheme. This is great news because it greatly simplifies euro payments with British clients or suppliers. In practice, you have a market of 36 countries where your payments move as if they were domestic.

What happens if I get the IBAN wrong?

It is a classic mistake and it has happened to almost all of us. Fortunately, the system has its own safeguards. If you get the IBAN format wrong (for example, you leave out a digit), your own bank will notice immediately and will not even let the order go through.

Now, if the format is correct but that bank account does not exist or is closed, the money will travel to the destination bank. There, when they cannot find where to credit it, they will return it. Be careful, because this round trip can take several days and some banks may charge you a small fee for handling the return.

The best advice I can give you is prevention. Check the IBAN twice before pressing the confirm button, especially if it is an important payment. A simple mix-up of numbers can cause delays and the odd cost you had not anticipated.

What is the maximum amount for an instant SEPA transfer?

The official limit set for instant SEPA transfers is 100,000 euros per operation. This allows you to send a considerable amount and have it arrive at its destination in less than 10 seconds.

However, it is essential that you know something: each bank can set its own limits, and they are usually lower for security. So, if you are planning to send an instant payment for a high amount, the smartest thing to do is to check your bank’s conditions first so you do not get a surprise.

With the right tools, managing your SEPA bank transfers no longer has to be a tedious task. At ConversorSEPA we are dedicated to exactly that: enabling you to transform your payment files into a validated XML format in minutes, saying goodbye to errors and saving hours of work. Try our solution and optimise your payment processes today.